{kind=link}

The BRRRR strategy is one of the best ways to build wealth in real estate investing. What is it and how does it work, you ask? Read on to find out.

What Is the BRRRR Strategy?

BRRRR is an acronym that stands for Buy-Rehab-Rent-Refinance-Repeat. As the last R suggests, real estate investors often implement this strategy multiple times over their career. It is a unique framework that represents a hybrid between active and passive income. When done right, you can build a rental property portfolio without using up all your money or running out of cash!

Essentially, you buy an investment property below market value and fix it up. The rehabbed property is then rented out to tenants to generate rental income that enables you to pay the mortgage, earn profits, and build up equity over time.

Once a sizable amount of equity in the property is built up, you refinance it to buy a second investment property, and so on. If done right, you can pull most (or even all) of your original capital back out for the next deal.

As you can see, the point of the BRRRR strategy is to help real estate investors acquire and build a portfolio of passive income rental properties without having to save up for a down payment for each investment property. No, it’s not a get-rich-quick scheme, but it’s a great way to get started in real estate investing and buy multiple properties when you do not have cash available.

Related: How to Buy Multiple Rental Properties in a Single Year

How the BRRRR Strategy Works

Let’s go through each component of the BRRRR strategy and break down how it works.

B Stands for Buy

The first step of the BRRRR strategy is to find and buy a property that is undervalued and has some upside potential. When searching for an investment property for sale, remember that the goal isn’t to flip it. Instead, you want to hold onto the property by turning it into a rental.

So, make sure the property you buy represents a sound investment deal and can perform well as a rental property. Good investments can be difficult to recognize, but that’s why you should know how to analyze properties and work with real estate numbers.

Analyzing properties for the BRRRR strategy includes calculating the cost of rehabbing, estimating monthly rental expenses, and ensuring that the rental income will provide a sufficient profit margin.

Many real estate investors use the 70% rule, which estimates the cost of repairs and the after repair value. The 70% rule helps you determine the maximum offer to make and ensures that a profit margin will remain after renovating the investment property.

It doesn’t really matter how you buy the property. Whether you pay cash, take out a mortgage or a hard money loan, you can use the BRRRR strategy. However, many recommend using a hard money loan. Banks don’t like risk, and deals that need work are risky.

By using cash or hard money, on the other hand, you can buy property that is a bit risky so you can add value. Then, you can refinance with something long term like a mortgage. Just be sure you have enough cash on hand to purchase the investment property plus fund the renovations.

Looking for cheap properties for sale in your housing market? Mashvisor will help you analyze and find the best deals in a matter of minutes using innovative tools.

R Stands for Rehab

The idea is simple – after buying the investment property, fix it up in a way that increases its value and makes it livable. Keep in mind that you don’t have to rehab a BRRRR rental property the same way you’d rehab a fix-and-flip. Instead, because you’re looking to make cash flow from the BRRRR strategy, focus on necessary renovations that add to the amount of rent you can charge.

Also, avoid investing in renovations that will cost you more than what can be produced through rental income. Some examples of good home improvements that’ll increase your property’s value include fixing the kitchen with reasonably priced additions, changing the carpet, and painting.

Here are 6 Rental Renovation Tips to Know Before Spending Any Money

Rehabbing also needs to be done in a way that doesn’t consume all of your time. Time is money for real estate investors. The longer it takes to rehab the investment property, the longer it’ll take to get your money back and buy another one.

A good contractor will help you save time and money so you’ll be able to get the most bang for your buck in terms of a rehab. Once your renovations are finished, you’re ready to move on to the next step of the BRRRR strategy.

R Stands for Rent

In order to refinance a rental property, banks want to see that it’s generating income. So, once the rehab phase is complete, the real estate investor needs to get the investment property rented. There are a few things to consider in this phase in order for the BRRRR strategy to work:

1. Finding Good Tenants

First, you need to find good tenants who will pay market (or higher) rents. How do you find good tenants? Well, there are no guarantees, which is why it’s extremely important to screen tenants diligently and do the following:

- Get their social security numbers

- Do a background check

- Ask for contact information for previous 2 or 3 landlords

- Verify the tenant’s job and income

- Have a written lease or tenancy agreement

2. Managing the Rental Property

Should you hire a property manager or manage the property yourself? Of course, this is a personal decision, which mainly depends on whether or not you have what it takes to become a landlord.

Managing a residential rental property requires finding tenants, collecting rent, and taking care of maintenance and repairs. Most of the time, it might be best to have a property manager do all of this work and, thus, make your rental income passive.

But, if you’re still considering managing the investment property yourself to save money, we’ve prepared this guide that’ll teach you all you need to know: Residential Property Management: Here’s How to Do It Yourself.

3. Generating Positive Cash Flow

Finally, you want to make sure that the investment property will generate positive cash flow in order for the BRRRR strategy to work. The more money the rental property makes every month, the more likely the bank will lend to you. It means your rental income needs to cover all of the monthly expenses, including the mortgage payment, insurance (respectively, rental property insurance or commercial landlord insurance), and property taxes. But how do you estimate how much to charge for rent?

There are a number of methods that real estate investors use to calculate monthly rent. For example, there’s the 2% rule, which says that for a rental property investment to be good, the monthly rent should be equal to or higher than 2% of the total cost of the investment.

Say, you’ve purchased an investment property for $60,000 and put $20,000 into rehabbing it, making your total investment $80,000. Following the 2% rule ($80,000 x 2% = $1,600). This is the monthly rental income you need from the property to generate positive cash flow.

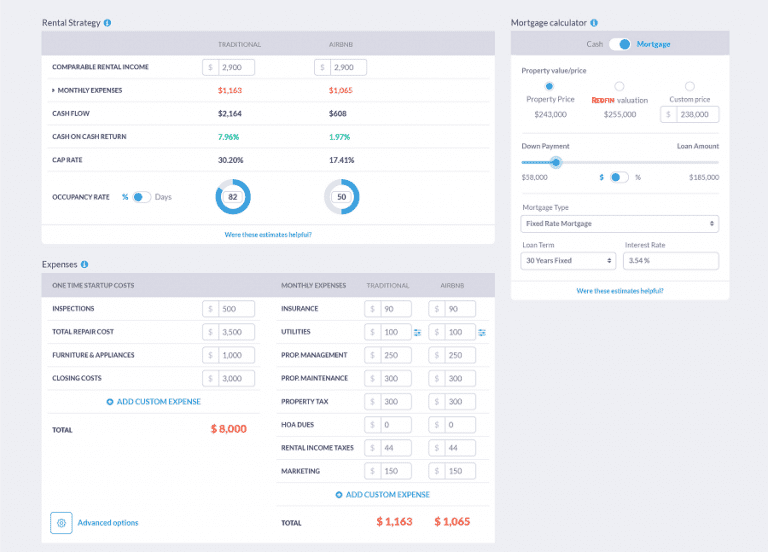

An easier way to find if a rental property will make positive cash flow is by running the numbers on an investment property calculator. The tool provides a comparable rental income based on real estate comps. In return, it enables you to see if the investment property will give you positive cash flow before even buying it once you plug in your expected rental expenses.

Mashvisor’s Investment Property Calculator

R Stands for Refinance

The next step to completing the BRRRR method is refinancing the property. The goal is to get your money back so you can repeat the process, which makes this step the most crucial in this real estate investment strategy.

Some banks will offer a cash-out refinance, while others will only offer to pay off outstanding debt. Of the said options, you want to select the first. You should also ensure that the bank will provide a loan on the appraised value of the rehabbed property (not on the original value of the property before the rehab).

Moreover, many banks will require a seasoning period which indicates how long the real estate investor must own the investment property before refinancing. A typical seasoning period is at least 6 months or one year of ownership.

In addition, a real estate investor can refinance a property for 75% of the appraised value. So, an appraiser will appraise the value of your rental property. After the appraisal is completed, the bank will lend you 75% of that value and will give you cash-out refinance. For example, say you

- Buy the property for $60,000

- Rehab it for $20,000

- Rent it out for $1,600

One year later, if the investment property appraises for $120,000, the bank will let you refinance and take out a $90,000 loan. Usually, it takes about 30 – 45 days for the loan to be processed.

R Stands for Repeat

The last step in the BRRRR strategy is to repeat the process after receiving the cash from the refinancing. Real estate investors can use this cash to buy and rehab another investment property.

Your first purchase will be the hardest, but after that, you’ll have the experience and knowledge to tackle your second, third, fourth property, and so on. Just repeat the cycle to grow and build a portfolio of positive cash flow rental properties and multiply your income without tying up cash.

To start looking for and analyzing the best investment properties in your city and neighborhood of choice for the BRRRR strategy, click here.

The Pros and Cons of the BRRRR Strategy

Real estate investors need to know several things about the BRRRR strategy before putting cash on the table. Here are the pros and cons of the BRRRR real estate investing strategy:

Pros

1. You Get Your Cash Back

One of the significant benefits of the BRRRR method is that after completing the renovations, you can refinance the investment property based on its after-repair value (ARV), instead of its purchase price.

It means you can not only withdraw all the initial cash you put in, but in some instances, you can even pull out more cash. That makes it a lot easier to purchase your next rental property!

2. You Can Finance the Renovation Costs (Usually in Full)

Most fix-and-flip lenders or hard money lenders will finance 100% of your renovation costs. That’s the good news. For the bad news, you can usually be reimbursed on a draw schedule. It means you need to shoulder the initial cost for each phase of the renovation, then the lender will reimburse you for what you spent on that work.

So, you need some operating capital, but you don’t need to cover the entire renovation cost of your investment property yourself.

3. Forced Appreciation and Equity

Many real estate investors prefer renovation projects because they can purchase an investment property at a discount, put in the renovation work, and create “forced appreciation” and equity by improving their property. For example, you buy a property for $100,000, spend $25,000 on repairs, and end up with a property worth $200,000.

You can predict the numbers up to a certain extent. You know your purchase costs and renovation costs (assuming there are no hidden costs), and you get a strong sense of the ARV (especially by using Mashvisor’s market research data!).

However, it doesn’t mean that the process will be problem-free, but it’s far easier to predict the returns on an investment property and renovation project than, say, a stock’s returns.

4. The Final Product Is a Long-Term Investment Property in Excellent Condition

When real estate investors complete the renovation process, they know the exact condition of the property’s every component.

Since they’ve replaced or updated many of the components, they know they can expect them to last for a longer period of time. A brand new furnace is far less likely to stop working than a 15-year-old furnace!

Still, real estate investors who engage in the BRRRR strategy should set aside money for capital expenditures, repairs, and maintenance, just like any other landlord. There’s nothing worse than a $5,000 repair bill and only $1,000 in your operating account.

Cons

1. You (Probably) Must Deal With Two Rounds of Closing Costs

Notice that third “R”, which stands for “refinance”?

It means a second round of closing costs with a second lender. With the second lender, you will need to pay another round of fees and put in another round of title work, etc. In other words, you’ll be out of pocket by thousands of dollars in new fees.

Unfortunately, real estate investors don’t enjoy many options to get around the second round of financing costs. Some lenders offer a single loan with two phases: a higher-interest renovation phase and then a lower-interest long-term renter-occupied phase. Whenever possible, rental investors should opt for such types of loans.

2. The Temptation to Overleverage

There might come a time when you would be tempted to take out several loans and assume a heavy debt burden.

If you invest $75,000 to purchase and renovate an investment property, and a long-term lender offers you $100,000 when you approach them to refinance, it’s hard to say “No thanks, I’d just like the $75,000.” The offer can be very tempting, especially when you’re low on cash for your next investment property.

But where does the cycle end? It doesn’t – you just end up with a series of overleveraged investment properties with less than ideal cash flow.

When you first acquire a property, you purchase it with cash flow projections in mind. Make sure to stick to your original cash flow projections, so that each property in your portfolio generates strong cash flow on its own.

3. The Rush to Refinance Can Lead to Hasty Leasing

Often, before finalizing the refinance loan, long-term lenders would like to see a signed lease, with tenants occupying the rental property.

Even when the refinance lender does not require so, many real estate investors feel squeezed by the high-interest renovation financing that they jump in immediately to sign a lease with the first applicant

Keep in mind the quality of the renters significantly influences the quality of the landlords’ returns. You need to be thorough and patient with screening your prospective tenants and be disciplined to say “no”, even with a high monthly payment hanging over your head.

4. The Risks Inherent in Relying on a Refinance

What happens if your investment property doesn’t obtain a high appraisal enough to secure the refinance?

Remember that short-term renovation financing is not only expensive, it’s also short-term. It can be challenging if your renovation loan comes due, but no long-term financing is forthcoming.

Some lenders impose seasoning requirements or other provisions that you might not have anticipated. Fortunately, it’s easier than ever to secure long-term financing as a real estate investor, with the growing number of online investment property lenders.

Alternatives to the BRRRR Strategy

You can pursue other real estate investment strategies if you decide the BRRRR strategy isn’t the one for you. One option is renting out a property that you purchased in exchange for rental income. The rental income from the property will help you pay for the existing mortgage or other expenses that you deem necessary.

Another method is real estate crowdfunding, which involves investors pooling their funds together to make equity investments in residential (or commercial) properties. Real estate crowdfunding comes with a lower barrier to entry, making it very accessible to investors with limited capital.

House wholesaling is another option for investors. It involves wholesalers buying undervalued properties from sellers and finding buyers to sell the investment properties at a higher price point. Acting as a middleman, you can make money by charging a wholesale fee on each transaction, which is typically a percentage of the total property price.

Wrapping Up

As you can see, the BRRRR strategy is a solid way to build wealth from rental properties. But of course, you need to be smart and plan correctly just like with any other real estate investment strategy.

If you’re looking for cheap properties for sale so you can get on the BRRRR strategy, sign up for a 7-day free trial of Mashvisor, followed by a 15% discount on your subscription.