{kind=link}

Real estate. How real is it for you? What most people don’t realize is that every single one of us is connected to real estate in some way or another. At some point or another, people are looking to rent or buy homes. Think of all buildings in the world, from that mini-market by the corner to the Empire State Building. All bricks and mortars are real estate and without bricks and mortars, we’d have nothing but mother nature.

If you’re sick of hearing about the housing market and not understanding what the heck everyone is talking about, then consider this guide as the North Star, leading you to the common knowledge of real estate. Here’s to gaining the real estate shrewdness you need in order to buy or sell a house, or just have a basic understanding of market conditions.

Important Real Estate Terms

Lesson one, vocabulary.

- ABCs of Housing – there are 3 different categories of housing.

- A – luxury homes

- B – middle-income homes

- C- low-income housing

- Adjustable Rate Mortgage (ARM): a type of mortgage loan where the interest rate on your balance or mortgage note changes, or adjusts over a period of time. There is usually a benchmark of which the interest rate changes, and it does so periodically.

- Fixed Rate Mortgage: unlike ARM, Fixed Rate Mortgage is a type of mortgage loan in which the interest rate remains fixed or unchanged throughout the entire term of the loan.

- Escrow: Here comes the legal lingo. Escrow is a deposit of cash held by a third party (Escrow officer) while a buyer and a seller complete a deal. If everything goes smoothly during the closing stage of the transaction, the cash in Escrow is transferred to the seller and home-ownership for the buyer is finalized.

- Lien: is a legal right granted to a property seller which acts a security against money owed by a buyer. Lien secures the seller against loss.

- Pre-Approval: occurs when a lender evaluates a borrower and determines whether or not the borrower qualifies for a loan from them. The evaluation takes into account a borrower’s income, expenses, and general credit check.

- Contingency: in real estate, contingency simply means that there are some terms and conditions that need to be met for a property before a deal or a sale is made. This can include financial contingency, appraisal contingency, sale contingency, inspection contingency, among others.

- Appraisal: valuation of a property. Appraisals are helpful because they aid in determining the value of the property at the time of sale or purchase, and are also beneficial for tax purposes. There are different methods a property is evaluated including the Current Market Value (CMV) as well as different valuation models.

- Closing Costs: these are expenses paid by the home-buyer at the closing or end stage of a real estate deal. Examples of closing costs include attorney fees, appraisal fees, inspection fees, origination fees, among others.

- Title Insurance: a type of protection against losing property ownership from legal issues. Lender’s title insurance is the most common title insurance, which is paid by the borrower of the loan, but protects the lender.

- Buyer’s Agent: is a real estate agent who represents the buyer in a real estate transaction. There is usually a binding contract between the buyer and the agent. A buyer’s agent helps the buyer look for property, researching the area, and eventually negotiating the price of the property with the seller.

- Listing Agent: is a real estate agent who lists home on the multiple listing service or MLS and helps homeowners market and sell or lease their homes. They negotiate prices and terms of sale on behalf of the seller.

- Realtor: is a real estate agent who is a member of the National Association of Realtors and are subscribed to its Code of Ethics.

- Broker: is a real estate agent who has acquired special education and who has taken and passed a broker’s license exam. A real estate broker acts as a liaison between a home-seller and a home-buyer when they’re attempting to make a deal.

- Earnest Money Deposit: is a deposit made by a buyer to a third party intermediary to show that the buyer is serious about the property purchase. The money is usually held in an Escrow account. When the deal is made, the deposit is added to the buyer’s payment for the property. If the sale falls through, the deposit can either go to the buyer or seller, depending on the terms of the purchase agreement signed.

- Private Mortgage Insurance (PMI): is an insurance policy which protects the lender against loss in the case the borrower cannot fulfill their mortgage payments. Buyers are usually required to buy a PMI if they put pay a down payment that is less than 20% of the house’s value. If indeed the buyer defaults, the lender repossesses the house and sells it.

- Gentrification: simply put, gentrification is defined as the process of renovating and renewing a house, neighborhood, or district. Gentrification is often used with a negative connotation; however, it provides real estate with countless opportunities.

How The Housing Market Works

In this section, you’re gonna learn the good stuff. You know how people complain when the housing market is down? Or when they say now is a great time to sell or buy? Then you just nod without really understanding what this all means? This section outlines the different dynamics that affect the housing market (why things change) and what these effects mean. Think of the housing market as two separate tiers.

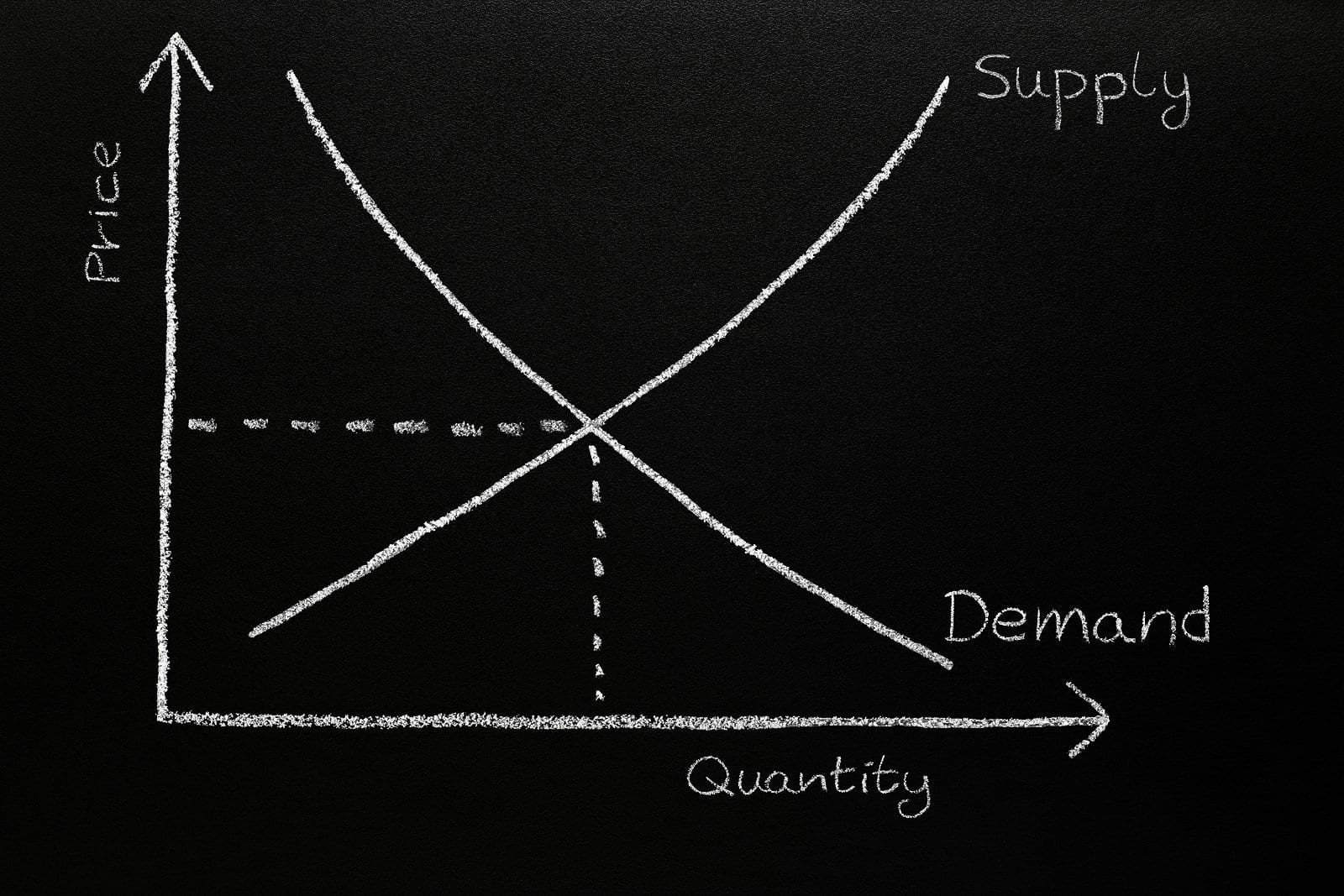

- Supply and Demand

It’s all about supply and demand

Relationships are about give and take, and real estate is about supply and demand. The rule of supply (houses for sale) and demand (people wanting homes) is the foundation of how the real estate housing market works. When the supply of homes is more than the demand, home prices decrease.

Why do supply and demand change? These are the drivers:

Supply

- Upgrades: People sell their homes in order to buy bigger and more expensive homes, adding to the supply.

- Construction: When more homes are built, inventory increases.

- Owners go back to renting: more home available when people sell their homes in order to start renting a property elsewhere. For example, retirees sell their homes and usually relocate as renters.

Demand

- Employment: if an area has a lot of jobs, people will come to that area.

- Population: as the population increases, more people need homes.

- Income: if people are making money, they are able to buy homes.

- Mortgage and interest rates: if people are able to qualify for a loan and afford the rates, they are more likely to buy.

- Trends: if buying a second property is becoming a trend, demand will increase. For example, in 2004, buying a second property was very popular among baby boomers.

What do supply and demand actually affect?

- Home appreciation

- Buyer and seller behavior

- Sales

Let’s look at how these three things change when demand is higher than supply (seller’s market).

- Home appreciation: Home prices increase rapidly and sellers are able to make to make huge returns on their property.

- Buyer and seller behavior: Sellers become eager and willing to sell homes while buyers either 1) rush to buy a property before prices increase or 2) wait out the storm and wait for prices to go down.

- Sales: Homes sell quickly, sellers can receive multiple offers, and the selling price is more than the asking price (due to bidding wars).

Let’s look at how these three things change when supply is higher than demand (buyer’s market).

- Home appreciation: Home prices decrease and buyers are able to get good deals.

- Buyer and seller behavior: Buyers become eager to buy while sellers aren’t as eager because they’re likely not getting the price they want.

- Sales: Homes sit on the market longer, sellers don’t receive a lot of offers, and the selling price is less than the asking price.

Supply and demand also decide if it’s a buyer’s market or seller’s market. Let’s dive deeper into those two terms in the next section.

Buyer’s Market vs. Seller’s Market

Now that we understand what supply and demand mean and what actually drives them, let’s move on to the second tier. The status of supply and demand determine if it’s a buyer’s market or seller’s market.

Seller’s Market

If there is a higher demand than there is supply, then it it is a seller’s market. Since sellers have something that everyone is fighting over, you can imagine why home prices increase in a seller’s market. These are the main features of a seller’s market:

- Less properties are listed – about 3 months or less worth of inventory is on market

- Properties spend less time on the market

- More closings

- Rising prices

What happens to buyers in a seller’s market? The first question that might come to mind is, “should I even buy a home when it is a seller’s market?” The answer is, yes, if that’s your goal. If you want a house of your own, then you can’t really put that off until it’s a buyer’s market because a seller’s market can last for years – it’s a huge unknown.

How does a buyer survive in a seller’s market? Good offers. First of all, understand that competition is fierce and things will move quickly. Sellers usually get multiple offers in one day, and listed homes can even be sold the day they’re listed. Second of all, most offers are above the asking price. In order to be able to put in a good offer and negotiate well, you need to:

- Get pre-approved for a loan

- Know and organize your financial situation

- Act quickly

- Make a strong offer

- Consult an expert when offering

Buyer’s Market

If there is a lower demand, than there is supply, then it is a buyer’s market. If there are plenty of houses for sale, and not as many buyers, then buyers are able to be more selective and get better deals on properties. These are the main features of a buyer’s market:

- More properties are on the market, 6 months or more of inventory

- Properties spend more time on the market

- Less closings

- Falling prices

If it’s a buyer’s market, should you not sell? What if you’re moving or are ready to sell your investment property? If you are trying to sell your property in a buyer’s market, the first thing to know is that buyers are going to be picky (more so than usual). The best way to handle this is by being willing to compromise. Obviously, in a buyer’s market, there are plenty of houses on the market, so a seller must have an edge in order to compete. How to compete? Strategic marketing to niche markets. Don’t just list the house, put the listing in front of tenants that the property would appeal to the most. Of course, if the property doesn’t sell, you can always rent it out.

Let’s talk about the benefits of being at the right place at the right time. If you are buying a property during a buyer’s market, there are a lot of different options to explore and many opportunities to negotiate a great deal. However, as we all know, having too many options can actually be daunting. Write down the most important qualities to you and narrow down properties based on that list. This doesn’t mean you’ll get everything on your list but it does mean you’re likely to find a property faster.

If you’re selling a property in a seller’s market, you’re going to make bank. This is a time when you’ll truly be able to benefit from home appreciation. This doesn’t mean you should list the property at a ridiculous price and expect to get the amount in full. On the contrary, be logical when it comes to pricing but also persist when negotiating.

Neither Seller’s Market or Buyer’s Market

There is something called a transitional market, when the conditions aren’t necessarily better or worse for buyers or sellers. This is when supply and demand are almost equal to each other, which causes pricing to stabilize. This occurs as the market transitions from one market to the other.

No matter what the market cycle is (buyer’s or seller’s), eventually it comes to an end. Buyer’s market and seller’s market can lasts from months to years but neither market will remain constant forever. These two factors explain why neither cycle can last forever:

Related: 6 Benefits of Investing in Income-Producing Properties

- Cause and effect. When things are going well for an area, everything else falls into place. The contrary is also true. When the economy suffers, the housing market suffers. As an example, a flourishing job market leads to high appreciation rates while a poor job market leads to prices dropping, high vacancy rates, and properties sit on the market for a long time.

- Historical trends. What goes up must come down. Since the housing market is all about cycles, conditions don’t last forever, and they eventually go back to the conditions that preceded it. Just like the transitional market, remember? For example, when home appreciation rates are on the rise, home prices eventually stabilize or decrease. These cycles help professionals forecast future trends, and now you can too.

Why The Housing Market Gets More Complicated Than Supply and Demand

Now that we understand what supply and demand is, let’s understand why each city’s housing market varies and why the cycle is in fact, imperfect.

- Buying homes is a seasonal thing. believe it or not, people aren’t always looking to buy houses. In the colder states, sales pick up in the spring and decline in the fall. During the winter, buyers aren’t looking to move during the cold, which is why selling a home is difficult during that time.

Related: The Best Time for Buying Real Estate Investment Properties

- Steps on the housing ladder. The purchases and sales of homes are based on different generations and where they are in their life. When retirees downsize or relocate, they sell their homes, making properties available to move-up buyers, who also sell their homes, making properties available to first-time home buyers. However, when first-time home buyers don’t buy properties, that leads to a domino effect of older generations unable to sell their homes.

- Market conditions. We keep seeing this phrase a lot. What are market conditions? They are basically the characteristics of an area, which affect how things work in real estate. An area’s schools, crime rate, amenities, transportation, for example, later affect how people move in or out of the area, which affect how houses are bought and sold and so on and so forth.

- Worn-out properties. Not all properties are able to appreciate and give their owners the profits they’re looking for. An A-category house or building can fall into a lower category because it has been worn out.

What Are Foreclosures?

One of the most common mishaps that homeowners go through is foreclosure. This word might send shivers down your spine, it might get you excited, or it might just confuse you. The housing market can have its cycles and do its thing, but every home is different and every homeowner has a unique situation.

It’s important to understand what foreclosures are and how they occur because 1) it provides insight as to how to avoid falling into foreclosures and 2) presents opportunities.

A foreclosure property is a property in which the homeowner is unable to make their loan payments and the bank tries to make their money back by finding another buyer. There a few steps that lead up to this occurring.

1. Missing Payments

Mortgage payments are usually due the first of the month and many banks give a grace period until the 15th of the month. If a borrower has missed a payment and the grace period, then a bank sends a notice and there is usually a late fee. Missing at least one mortgage payment is referred to as payment default.

If a second payment is missed, a more serious letter is sent, usually a Demand Letter. The lender or bank will try to figure out a plan to make up for the missed payments.

2. Notice of Default

A notice of default is sent after 90 days of the missed payments. The homeowner (borrower) is informed that the letter is recorded and the letter is sometimes delivered at the property. Usually the homeowner is given another 90 days to sort things out; this period of time is referred to as the reinstatement period.

3. Notice of Trustee’s Sale

After the Notice of Default is issued and no payment has been made during the reinstatement period, it’s time that the property goes up for auction. A Notice of Trustee’s Sale is sent, which is a letter and notice that announces a public auction and includes the related information. A Notice of Foreclosure Sales is also sent to the borrower, which a signed order by a judge, stating that a Notice of Sale should be published and the owner sells the property at the auction.

An auction is then taken place and the property is awarded to the highest bidder. The Trustee’s sale is completed and then the buyer receives a Trustee’s Deed Upon Sale.

4. Bank-Owned

If the property does not get sold during the auction, the lender (bank) becomes the owner and has to sell the property on their own. The properties are referred to as bank-owned or real-estate owned (REO). The property is usually sold with the help of a broker or a REO Asset Manager.

5. Eviction Notice

The borrower can stay in the property up until the property is sold. At that point, an eviction notice is issued, which states that everyone and their belongings have to leave the property.

How do people fall into foreclosures? It’s easy to assume or judge that borrowers are irresponsible and that’s why they’re unable to make the payments. But that’s not always the case. There are several possible scenarios such divorce, losing employment, relocation, or not putting a large enough down payment.

It’s hard on families to leave their homes. Fortunately, the bank usually tries to work out a solution with the borrower, but it’s also important to know what to expect and how to act if the foreclosure is inevitable. There are several things you can do to save your home from foreclosure.

Related: How to Buy a Foreclosure as an Investment Property

Misconceptions Of Real Estate

Finally, we have to address the some of the misconceptions when it comes to understanding or analyzing real estate and housing markets.

Hyper-locality

When looking at housing market averages, you’re usually looking at country averages. Unfortunately, country averages are a misrepresentation because market conditions can greatly differ just from neighborhood to neighborhood and property to property.

Price = Value

No! What a person pays for a house is not necessarily what the house is worth. Prices are current and values are long-term. What does that mean? A house’s price is based on supply and demand, as mentioned earlier. The value of a house changes much slower than a price does. An appraiser decides what the property but that does mean they take into account the prices of the property the past six months.

You Need a 20% Down-Payment To Buy A HOuse

Don’t think for a second that every person who has ever bought a house had a 20% down-payment. No, there are plenty of home buyers and investors out there that bought houses without putting that much money down. Yes, there’s always a catch, but not necessarily bad. Those applying for a loan allowing them to put less than 20% down must have good credit, and might have to pay a PMI (scoll to the top if you forgot what that is).

How Real Is It Now?

Hopefully you’ve gained the basic understanding of what real estate is, how the housing market works, and its complexities. Supply, demand, buyer’s and seller’s market are all terms that hopefully have deeper meanings to you now. What’s the next step? Learning about mortgages is a whole other entity in itself. Invest time in understanding different mortgage plans and how to select the best plan.

Congratulations, you can now have an informed conversation about real estate and more importantly, make better decisions in the future.