{kind=link}

You’re ready to purchase a real estate investment property, but you want to do an ROI analysis before you close the deal. What is ROI analysis? The return on investment analysis is exactly what it sounds like: it is the process of evaluating the performance or efficiency of an investment by calculating the ratio between the gains and cost of the investment.

Though it seems like a simple equation, analyzing ROI in real estate is not always as simple as it sounds. This is because there are lots of numbers that real estate investors use when calculating ROI on rental properties. And with so many guides out there on the real estate ROI and how to calculate it, some might get confused and start to make mistakes when analyzing investment properties. This is, by far, the worst thing that could happen to an investor as he/she might end up making a huge investment decision based on wrong estimations!

We’ve heard many stories from beginner investors saying they’ve bought an income property after an ROI analysis showed it’ll be profitable when, in reality, it wasn’t worth the investment. If you don’t want this to happen to you when investing in real estate, then you need to avoid the mistakes others have made in their ROI calculations. Wondering what these mistakes are? Keep reading to learn 5 commons mistakes real estate investors make when running the numbers and how to avoid them for an accurate ROI analysis before buying a rental property.

To learn more about how to perform ROI analysis, read: How to Calculate ROI in Real Estate.

Mistake #1: Using Estimates Instead of Actual Numbers

When beginner investors start to educate themselves more about the real estate investing business, they find that there are rules which are used as guidelines for whether or not to buy a particular property. For example, there’s the 1% rule which states that the monthly rent should be equal to or greater than 1% of the total purchase price of an investment property. There’s also the 50% rule which states that 50% of the rent you collect from a property will go towards expenses. So before buying a property, some would ask: does it meet the 1% rule or the 50% rule?

The first mistake some beginners make is using these rules for actual evaluation rather than as guidelines. Here’s an example to better understand what I mean: say that you’ve found a rental property for sale that meets the 1% rule. Great, now you should drop the rule and find the actual monthly rent of this property. You can do that simply by asking the seller how much rent current tenants are paying. If there are no current tenants, have a real estate agent or a property manager run a comparative market analysis to determine what rental comps in the area are renting for.

Your ROI calculation should be based on actual numbers because estimations can be hugely misleading. Again, these estimations are good only as guidelines when looking at a potential income property. But when doing an ROI analysis, always use actual numbers to make an educated investment decision.

Mistake #2: Failing to Account for All Expenses

Many times, real estate investors calculate ROI on rental property and forget to subtract some expenses. This is another mistake because when it comes to making money in real estate, minimizing expenses is key to getting higher returns. Meaning, when you forget about or ignore an expense in your calculations, the resulting ROI will be higher than what you should realistically expect. In turn, you’ll end up buying an income property because the numbers look nice on paper and forget to budget for these rental expenses.

So, when you evaluate a real estate investment by running an ROI analysis, make sure to account for all the monthly expenses that you can expect once you own the property. For example, some investors forget about the money lost during times of vacancy. Unless your rental property is in a very hot housing market, you should always include vacancy rates in your calculation. Other expenses that you can expect include, but are not limited to, property taxes, insurance, repairs, and (if applicable) property management fees, homeowners’ association fees, and mortgage payments.

Related: 9 Rental Property Expenses Real Estate Investors Shouldn’t Forget

Another note worth mentioning is that, again, you should always find actual numbers for these expenses to include in your ROI analysis. You can ask the current owner what they pay in taxes or look it up on the county’s tax assessor website. Get a quote from your insurance company. Before hiring property management, ask how much they charge. Call the homeowners’ association and find out how much they charge. Get a quote from your mortgage lender on what your payment will be. The only costs that you can’t know for sure are vacancy and repairs, so you’ll have to estimate those.

Mistake #3: Confusing Cash Flow and NOI

It’s important for beginner real estate investors to understand that net operating income (NOI) and cash flow are two entirely different concepts, each with entirely different results.

Cash flow is the amount of cash income in a given period of time minus the amount of cash expenses in that same period. The NOI, on the other hand, equals all revenue from the income property minus all necessary operating expenses. While they seem similar, the main difference between these two metrics in real estate is that NOI excludes debt service costs (loan costs). Cash flow, however, is equivalent to NOI adjusted for the expense of debt service. Meaning cash flow can be calculated as NOI minus debt service costs.

Why is it important to understand this difference when calculating ROI in real estate? Because investors need to know which number to include as “gains from investment” in the ROI analysis. If you’re evaluating a property that you’ve paid for in cash, the correct approach is to base gains on the net operating income since you don’t have any debt to include in your expenses. However, if you’re using a mortgage loan to finance your investment property, then you should be using cash flow since it represents the total profit you’ll see at the end of the year from your rental property after paying debt costs. Failing to do so will lead you to the next mistake investors commonly make when performing ROI analysis.

Mistake #4: Using the Wrong ROI Formula

Just like we have two real estate metrics for calculating profits, there are two formulas for calculating the ROI on rental property: the cap rate formula and the cash on cash return formula.

The cap rate measures how profitable the property investment is by comparing the NOI with its purchase price. Meaning, if you plan to do an ROI analysis on an income property that you’re paying for in all cash, you should use the cap rate formula. The cash on cash return, on the other hand, is used to evaluate the performance of mortgage-financed properties by comparing annual profits with the amount of cash actually invested. Using the right formula will lead to accurate ROI analysis.

We have multiple guides about these formulas for calculating the rate of return with detailed examples to help beginner investors better understand the differences. To start learning, I recommend reading:

- Real Estate Investing for Beginners: How to Calculate Cap Rate

- How to Calculate Cash on Cash Return for Any Rental Property

- Cap Rate vs. Cash on Cash Return

Mistake #5: Not Investing in a Real Estate ROI Calculator

For beginner investors, calculating the cap rate and cash on cash return for multiple properties to decide which one to buy for investment can be tricky. If you end up with inaccurate results, you could invest your money in negative cash flowing property – and no investor wants that! The best thing you could do to avoid using the wrong ROI formula or the wrong ROI calculation is to use a Real Estate ROI Calculator. Also known as the Rental Property Calculator, this tool will run all the numbers for you using the power of AI and predictive analytics. Where can you find this tool? Right here on Mashvisor.

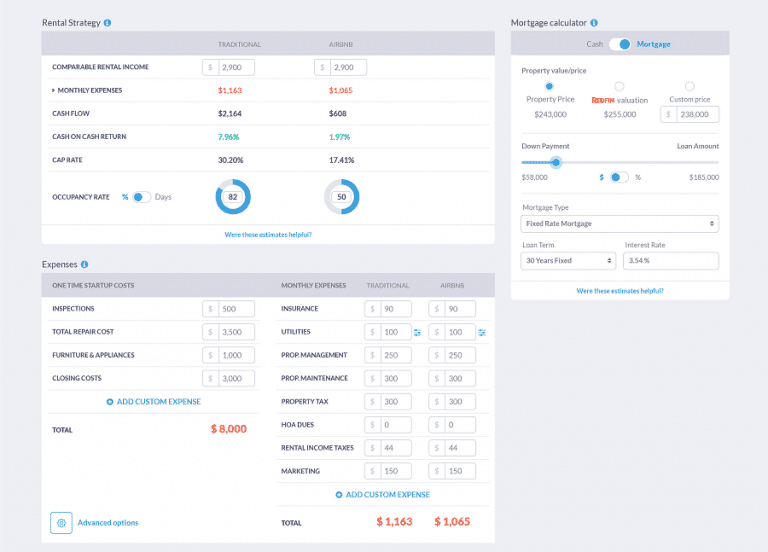

Mashvisor’s Rental Property ROI Calculator

Using Mashvisor’s Rental Property Calculator is easy. All you have to do is determine how you’re going to finance the property investment (cash or mortgage) and enter your financing details. The Rental Property ROI Calculator will then run an ROI analysis and show you both the cap rate and cash on cash return you can expect to earn from this rental property. It’ll also show you other readily calculated metrics to help you fully analyze the property’s profitability including rental income, cash flow, occupancy rate, as well as a breakdown of the rental expenses to account for.

Needless to say, our Real Estate ROI Calculator will help you choose your next investment property with the confidence you need to succeed in the business. To use the best Rental Property Calculator and start calculating ROI like a pro, start out your 14-day free trial with Mashvisor now!