{kind=link}

One of the advantages of being a real estate professional is its tax benefits. Learn the secret tips that can help you qualify for these benefits.

Real estate is a great option for investors to generate passive income and build long-term wealth. In fact, real estate investing is one of the best investment strategies because of its lucrative returns. Aside from earning generous profits, there are several other reasons why many people want to start their own real estate careers.

Table of Contents

- What Is a Real Estate Professional?

- How to Qualify as a Real Estate Professional for Tax Purposes

- Other Tax Rules You Should Know

- When Should You Become a Real Estate Professional?

- Tips to Qualify as a Real Estate Professional

Tax advantages are also a part of the perks of being a real estate investor. There are many options for reducing the taxes you’d normally pay on real estate income. With the right tax strategy, you could save thousands of dollars on taxes each year. But to effectively enjoy these tax benefits, you need to comprehend the tax rules related to investing in real estate.

Yet there are further subtleties to how the IRA taxes rental real estate revenues that regular investors may not be aware of. Knowing the different tax rules is crucial to being a successful investor. For one thing, being taxed as a real estate professional offers more advantages, but you need to be knowledgeable of the tax code first.

From the IRS’s point of view, becoming a designated real estate professional has a special tax advantage. But first, you need to know how to qualify as a real estate professional for tax purposes. In this article, we’ll discuss what makes an investor have real estate professional status and how to qualify as one.

What Is a Real Estate Professional?

From a tax perspective, a real estate professional is a status or designation you can choose when filing your tax return. By selecting this option, you can apply losses from your real estate activities to reduce your income. It includes income from sources like a regular job or owning a business. This practice can potentially help lower your tax liability.

Rental real estate investors can always deduct expenses and depreciation from their income. If you have greater rental expenses than your rental income, there are regulations that you need to follow. These rules determine whether you can utilize the real estate losses to offset income from other sources.

According to the IRS passive loss rule, you cannot deduct losses from passive activities from their taxable income. Based on the IRS, rental real estate investing is a passive activity. Thus, if you’re a regular investor, real estate losses cannot be used to offset W-2 wages.

The IRS, however, makes exemptions to this regulation:

- People with modified adjusted gross income (MAGI) below $100,000 are exempt from this passive activity loss limitation. They are allowed to deduct up to $25,000 in passive losses.

- Being a real estate professional makes you eligible for favorable tax treatment.

As a real estate professional, you are not limited in your deductions. Under this special status, the IRS considers your real estate revenue non-passive if you meet specific requirements. As a result, whatever your income level is, you can deduct all your real estate losses from your taxes.

Related: Is Real Estate a Good Career?

How to Qualify as a Real Estate Professional for Tax Purposes

A real estate professional, in the context of United States tax laws, is an individual who meets specific criteria set by the IRS. Many are wondering how to qualify as real estate professional for tax purposes. First, you must meet these IRS requirements and maintain documentation to prove that you meet them.

The IRS has specific standards defining what is required to obtain the designation of a real estate professional. Remember that the real estate professional tax status only applies to individuals. It does not apply to organizations.

Below are the real estate professional qualifications:

1. At Least 750 Working Hours in the Real Estate Industry

To qualify as real estate professional, you need to spend a minimum of 750 hours per year participating in real estate activities. These hours are only for work in the real estate industry. So you have to know what activities qualify for real estate professional status.

These activities include tasks such as property management and overseeing repairs and maintenance. You may also include tenant interactions and making important decisions related to real estate investments.

Plus, physically engaging in construction operations, promoting a property, and finding tenants for your rentals are all activities that count toward the 750-hour criteria.

However, investing activities such as doing research and finding for-sale listings do not count. If you’re managing rental properties, you must have an ownership stake of at least 5% for each rental property. You need this much ownership to qualify as a real estate professional.

Keep in mind that you and your spouse cannot combine your rental portfolio hours to meet the 750-hour minimum requirement. Each spouse must pass the real estate professional qualifications independently.

2. More Than 50% of Personal Services

You must spend more than 50% of your total working hours during the tax year doing real property trade or business. These activities include developing, constructing, acquiring, managing, and brokering real estate properties.

To meet this rule, the time you dedicate to real estate activities must exceed the time you spend on other jobs unrelated to real estate. Let’s say you have another job unrelated to real estate and work a total of 2,000 hours a year. You would need to devote at least 1,001 hours a year to real estate to satisfy this requirement.

Keep detailed records and documentation of your time spent on real estate activities. It supports your claim as a real estate professional. These records can include calendars, timesheets, project logs, or any other evidence. They should prove your substantial involvement in real estate work.

3. Material Participation in Each Real Estate Activity

You must materially participate in your real estate investments to achieve a real estate professional status. The real estate trade or firm which you materially participate in must account for more than half of your annual working hours. Therefore, if you work full-time, you won’t be able to qualify.

You can earn material participation by participating in real estate activities. These include active property management, acquisition, construction, reconstruction, or brokerage trade. You must perform these responsibilities continuously, regularly, and significantly. The IRS utilizes a 500-hour threshold to determine material participation.

As previously stated, hours spent on investment activities don’t count toward the 750 working hour threshold. But you can use them to satisfy the Material Participation Test. That is if you are directly involved in the portfolio’s day-to-day management.

Material Participation Rules

Do you want to know how to qualify for real estate professional through material participation? You must first understand the material participation rules and must pass one of these seven tests as follows:

- You must materially participate in real estate activities for more than 500 hours during a tax year.

- Your participation in these activities must exceed the contribution of other individuals involved. It doesn’t matter whether they are owners or not.

- You must participate in the activity for over 100 hours during the year. Ensure your involvement is greater than any other person’s participation, regardless of ownership.

- You must be significantly involved in the activity during the year, as defined by the tax regulations. Also, your total participation in all such significant activities in a year should exceed 500 hours.

- You must have materially participated in the real estate activity for five taxable years (consecutive or not). This is for the past ten taxable years.

- You must have materially participated in a personal service activity for any past three taxable years (consecutive or not).

- Your participation in the activity must be regular, continuous, and substantial. This is based on all facts and circumstances outlined in the regulations.

Other Tax Rules You Should Know

Aside from material participation rules, there are other tax rules that you should also know as a real estate professional. Here are the other two important tax rules that can help you determine if the real estate professional tax status is a good fit for you:

Passive Loss Rules

Passive loss rules are tax regulations that limit the ability to use losses from certain passive activities to offset income from other sources. According to the IRS, investing in rental real estate is passive. By default, losses from passive activity should only offset other passive income.

For example, if you have a rental property, you cannot use the losses you incur from this investment to deduct against your active income. You cannot use these losses to reduce income from a regular job, business, or assets in which you actively participate. This rule limits the potential tax benefits from a real estate investment.

Some exceptions and considerations allow you to deduct passive losses against other types of income. One of these is having a real estate professional tax designation. This is because real estate professionals operate in a real estate business full-time.

It means their income mainly comes from their real estate investments. With this, they can claim tax deductions using the losses they incur from real estate against all their income.

Note that qualifying as a real estate professional does not really provide tax benefits. To enjoy such advantages, you must prove that you materially participated in real property trade during a tax year. Revisit the material participation rules mentioned above to see how you can qualify for tax benefits.

Real Property Trade or Business Rules

These rules require you to participate in real property trade or business during the tax year. It is so that you can consider your real estate losses as non-passive. You need to have your own real estate portfolio to meet this requirement. Then you can deduct losses and expenses related to your real estate activities from all your income.

It means that the losses you incur from your real estate ventures can help reduce the taxes you owe on your total income. This includes the income from sources like a job or business unrelated to real estate.

According to IRS, there are 11 types of real property trades and businesses, as follows:

- Real property development

- Redevelopment

- Construction

- Reconstruction

- Acquisition

- Conversion

- Rental

- Operation

- Management

- Leasing

- Brokerage

It’s worth noting that professional services that are not directly related to real estate cannot be used to qualify as a real estate professional. For example, if you’re a lawyer specializing in real estate, you cannot use your professional service hours to qualify for real estate professional status. The same goes for accountants or tax professionals servicing real estate clients.

When Should You Become a Real Estate Professional?

We have just learned that being a real estate professional has more tax advantages. Yet, this does not mean everyone should apply for this tax status. Now that you know how to qualify for real estate professional status, let’s discuss when you should apply.

If you meet the following, then you should consider becoming a real estate professional:

You Own Many Rental Properties

The real estate professional tax status gives tax benefits for real estate investments. This is especially applicable to those who own large rental portfolios. As a real estate professional, you may be eligible for these benefits if you own several rental properties.

You can’t use the Real Estate Professional certification to offset all your income. But you may certainly use it to offset a significant portion of it. However, if you own only one rental property, your efforts may be in vain. In reality, a single rental property may not create sufficient losses to warrant this real estate professional status.

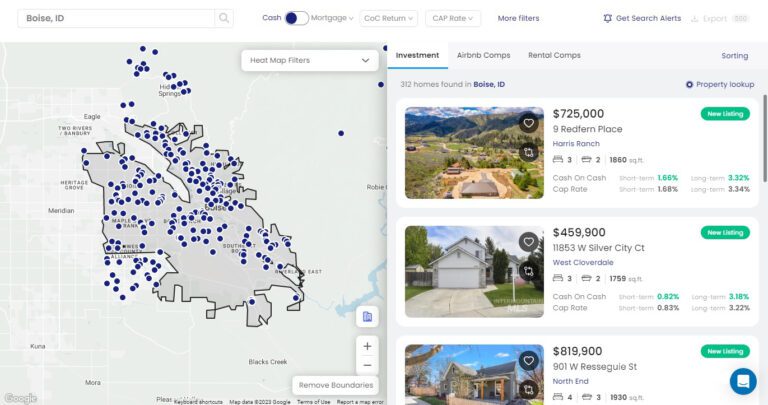

If you are planning to build your rental portfolio, you need to use effective real estate tools to help you find the best investment properties. You can easily do this with the help of Mashvisor’s Property Finder tool.

What Is Mashvisor’s Property Finder and How Does It Work?

Property Finder is a feature that helps you find the most profitable investment properties in your chosen location. All you need to do is type in the city or neighborhood of your choice, and you will see a list of properties for sale in that area. You can filter your search using different criteria to get more personalized results.

You can adjust your desired budget, property type, property size (number of bedrooms and bathrooms), and preferred rental strategy. Once you find a property that interests you, you can click on it, and you will see its complete details.

The best thing about this tool is that once you find a property you like, you will see an in-depth analysis of its investment potential immediately. You will see the estimated values for rental income, cap rate, cash on cash return, expenses, occupancy rate, and cash flow. What’s more, you get to compare both long and short term strategies to determine which is best.

On top of that, you can use the investment property calculator. It allows you to set your mortgage details, such as mortgage type, loan amount, interest rate, term, and closing costs. Through this, you’ll see how much you’ll pay in monthly amortization and whether the property earns enough cash flow to cover the mortgage.

Not only that, but you can adjust the expenses, occupancy rates, and nightly or monthly rates too. It allows you to get a more accurate computation based on your specific investment plans.

If you want to learn more about how Mashvisor works, start a 7-day free trial today.

Mashvisor’s Property Finder allows a real estate professional to look for investment properties anywhere in the US.

You Don’t Have a Full-Time Job

Based on the requirements of how to be a real estate professional, you need to spend a substantial amount of time and effort on this. So it’s easier to achieve the real estate professional qualification standards if you don’t have another full-time work.

In the real estate sector, any personal services you provide will be your only personal services. As a result, it will be easier for you to complete the 750-hour rule. The IRS takes this designation seriously. The IRS will audit those who appear unlikely to achieve the level of commitment required.

In other words, the IRS will find it suspicious if you make a lot of money as an actively practicing professional. It will question how you can spend more than half of your time managing your real estate assets. The IRS will disqualify those individuals who have other full-time jobs.

Related: Can I Invest in Real Estate With a Full-Time Job?

Tips to Qualify as a Real Estate Professional

Now that we have discussed how to become a real estate professional, the next step is ensuring you meet these qualification requirements. After all, earning a real estate professional status has numerous advantages.

Remember, meeting the criteria to qualify as a real estate professional requires a genuine commitment and active involvement in real estate activities. Since it is a difficult designation to obtain, you’ll need these practical tips to help you qualify as a real estate professional:

1. Time Dedication

Ensure you spend more than 50% of your total working hours during the tax year on real estate activities. To do this, you can take over more of the day-to-day management of your real estate portfolio. The time spent on this task could help you meet or even exceed the required minimum.

2. Meet the Hourly Requirement

Dedicate a minimum of 750 hours per year to real estate activities. Keep track of the time spent on various real estate tasks, such as property management, acquisitions, development, and brokerage. Take note of the acceptable real property trade and business categories and try to spend hours on those activities to meet your goal.

3. Active Participation

Actively participate in the management and decision-making processes of your real estate properties. Maintain records of your involvement, including attending meetings, making important decisions, and overseeing property operations.

4. Work Part-Time

Having a full-time job may not work if you want to be a real estate professional for tax purposes. If you could, find a part-time job that gives you more freedom and flexibility to work as a real estate professional. Consider how many hours you work and whether you could spend more than half of your free time managing your real estate trade or business.

Related: The Ultimate Real Estate Investment Strategies for Part-Time Investors

5. Involve Your Spouse

If you already have a full-time job and don’t want to leave, you can have your spouse apply. Of course, your partner has to actually do the work, not simply claim to do it. Make sure your spouse is on board with this plan. You’ll want to go over the IRS criteria carefully and make sure they are willing to take on this time-consuming responsibility.

6. Separate Activities

Separate your real estate activities from non-real estate businesses, jobs, or investments. This separation helps establish that you are primarily engaged in real estate. With this, you can claim tax benefits specific to real estate professionals.

7. Keep Detailed Records

The IRS wants to ensure you qualify as a real estate professional because of the significant tax benefits. Thus, they will audit your real estate documentation on a regular basis for enforcement purposes.

For this reason, it’s vital that you keep track of your working hours. You’ll need supporting paperwork to show that you worked 750 hours. You also need to prove that you spent over 50% of your working hours in real estate.

It’s easy to do this if you maintain detailed records of your time spent working in real estate and the tasks you completed. This is particularly significant for investors who also engage in other fields other than real estate.

Maintain calendars, project logs, emails, and any other relevant records and make sure they are accessible. These records serve as evidence of your substantial involvement and can support your claim as a real estate professional.

8. Professionalism and Business-Like Approach

Treat your real estate activities as a bona fide business. Keep separate financial records, maintain a dedicated workspace, and operate in a professional manner. Also, have a bank account dedicated to your real estate activities only. It helps make tax seasons smoother. Plus, you’ll also have more organized accounting.

9. Educate Yourself

Stay informed about tax laws and regulations related to real estate professionals. You can effectively plan and qualify as a real estate professional if you understand the requirements. Also, knowing the available tax advantages can help you maximize your benefits as a real estate professional.

10. Seek Professional Guidance

When in doubt, it’s best to consult a qualified tax professional specializing in real estate taxation. They can provide personalized advice and help you navigate the intricacies of tax laws. Moreover, they can help ensure compliance with the requirements for real estate professional status. Working with a professional can help make this complex process easier.

Are You Ready to Be a Full-Time Real Estate Professional?

If you meet the IRS’s requirements, you can qualify for real estate professional status. It means you’ll get to enjoy a slew of tax benefits. Are you thinking of how to become a real estate investor and want to maximize your income? Then you should consider acquiring a real estate professional status to take advantage of all the available tax deductions.

Now that you know how to qualify as a real estate professional, the next question is: are you ready to become one? Being a full-time real estate professional requires time, dedication, effort, and commitment to this venture. The good news is that aside from the tax benefits you can get, you’ll also enjoy lucrative returns from your investments.

Keep in mind, though, that not all investment properties will generate high returns. If you want to ensure profitability, it’s best to use a real estate platform to help you find the best markets that are optimal for your chosen investment strategy. To start on the right foot, be sure to subscribe to Mashvisor, and we’ll help you find the right investment properties for you.

Schedule a demo now to find out how Mashvisor works.