{kind=link}

The last time a flood of short sales was experienced was during the Great Recession of 2008 as homeowners lost their jobs and income.

Considering that many homeowners are experiencing similar challenges as a result of the impact of the COVID-19 pandemic, delinquencies are expected to be higher relative to last year, which means more of these sales will hit the market. Having said that, the COVID-19 mortgage relief for government-backed loans under the CARES Act has played a role in slowing this trend.

If you are looking to invest in short sale real estate in 2021, you need to understand how the entire process works. This guide explains the steps involved in investing in short-term sale real estate successfully. But before we dive into how to buy a short sale, we need to provide a brief short sale definition and go over some of the basic aspects of these deals.

What is a Short Sale in Real Estate?

A short sale occurs when a financially distressed homeowner sells their property to a third party for less than what they owe on the mortgage, pending the approval of the mortgage lender. After the sale has gone through, the lender takes all the proceeds from the sale and often writes off the difference between the original mortgage value and the sale price. However, this isn’t always the case. The lender may get a deficiency judgment against the homeowner requiring them to pay all or part of the remaining mortgage balance.

The short sale process usually happens when the homeowner can no longer make mortgage payments and their mortgage balance is more than their property’s fair market value due. This is generally caused by a decrease in property value. The homeowner has negative equity (ie, underwater) and needs to sell the property.

The mortgage lender will take a financial loss by allowing the homeowner to sell the property for less than the outstanding mortgage balance. Short selling may be a better alternative than foreclosing on the property because the foreclosure process could be more costly and time-consuming.

The homeowner applies for the short sale but the lender has to agree to it after conducting a thorough vetting process to prove that they can’t possibly keep up with mortgage payments. Therefore, homeowners will be required to prove financial hardship by providing documentation such as a hardship letter, pay stubs, and tax returns.

What are the Advantages of Investing in a Short Sale?

-

You can get a property below market value

Mortgage lenders typically prefer a short sale vs going through a foreclosure. This is due to the costs of maintaining the property before the sale and the risk of selling it for even less if it is in a declining market. Since lenders are highly motivated sellers, you can often get short sale real estate at discounted prices.

-

The property is usually in good condition

When it comes to buying off-market properties, one debate that real estate investors usually have is short sale vs foreclosure. One advantage of buying a short sale is that it’s often in a better condition than a property bought at a foreclosure auction. This is because the homeowner will still be occupying it and keeping up with basic maintenance. Conversely, foreclosed houses for sale are usually vacant since the occupants have already been evicted by the lender. Thus, they are likely to be neglected and in disrepair.

While buying a short sale has potential benefits, it comes with unique challenges. It is usually more complicated and more time-consuming than a traditional real estate transaction because of extra paperwork and the multiple lender approvals an offer needs to go through. It’s not uncommon for short sales to take up to a full year. These properties may also carry liens and unpaid taxes that you will be responsible for if you make a purchase without doing your due diligence.

How to Buy Short Sale Real Estate

If you have a flexible timeline, buying a short sale property can be a decent option. However, you need to approach it with caution. Below is our step-by-step guide to buying short sale real estate:

1. Find Short Sale Properties

Before you begin searching for short sale properties, it is a good idea to hire a real estate agent who has experience with short sale transactions. Real estate agents have access to the MLS, which is one of the most reliable sources of short sale listings. An experienced real estate agent will also help you prepare a competitive offer, negotiate the best deal, and guide you through the whole purchase process.

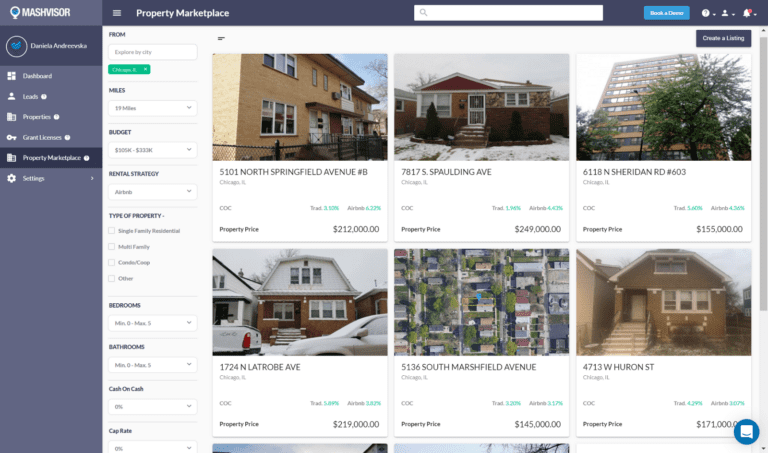

Use the Property Marketplace to find short sale real estate deals

Short sale properties can also be found in online real estate marketplaces like Mashvisor. The Mashvisor Property Marketplace is great for locating a variety of off market properties in the US housing market, including short sales, foreclosures homes, and REO properties. This tool allows you to quickly find properties that fit your criteria through search filters such as:

- Location

- Miles

- Budget

- Property type

- Rental strategy

- Listing type

- Number of bedrooms

- Number of bathrooms

- Cash on cash return

- Cap rate

2. Find a Mortgage Lender and Get Pre-approved

Unless buying a short sale property with cash, you want to find a mortgage lender and get a pre-approval letter. Shop around and compare different lenders to find one that is most right for your situation. A pre-approval letter will help you know how much you can afford to spend on a property. It will also show the seller’s lender that you are able and qualified to close, thus giving you the power to make a credible offer. When buying a short sale, you should be able to move quickly.

Related: What You Need to Know About Investment Property Mortgage Lenders

3. Do Your Due Diligence on the Property

Before you pursue a short sale property, it’s crucial that you conduct the necessary due diligence. This includes:

-

Home Inspection

Unlike regular property sales, a short sale is usually sold “as-is”. Therefore, it’s a good practice to conduct a home inspection and estimate the cost of needed repairs. Apart from the purchase price, you need to budget for these additional expenses. An inspection can help you uncover serious issues that may be deal-breakers. Therefore, skipping a home inspection can be disastrous.

-

Title Search

Since the seller is having financial problems, it would also be wise to check if there are any undisclosed liens on the property before you move forward with the transaction. Once you purchase the short sale property, you will be legally responsible for all liens on it. Do a title search to avoid any nasty surprises after closing. Also, consider getting title insurance to protect yourself against any undisclosed liens.

Related: Learn How to Do a Title Search in 5 Steps

-

Run the Numbers

Without evidence for the property’s value and positive cash flow potential, you are more or less gambling with your money. First, you should estimate how much the house is worth. The sale price must be in line with the property’s fair market value. To determine the fair market value, you need to research the price that other similar properties in the area have sold for in the recent past.

Secondly, if you are investing in real estate, you want to make sure that there’s rental demand and that you’ll have a good return on investment. You can easily conduct a comprehensive investment property analysis using Mashvisor’s investment property calculator. This tool will calculate key property metrics like rental income, cap rate, cash on cash return, and Airbnb occupancy rate in just a matter of minutes. If you want to flip the property, you will need to determine the after-repair value to know if it’s a profitable deal.

Related: Due Diligence in Real Estate: 9 Crucial Steps

4. Submit a Competitive Offer

Make an offer on a short sale

If you are convinced that the short sale house is a profitable one, the next step is to make a competitive offer. Your real estate agent will guide you through this process. However, keep in mind that making a low-ball offer may not work out in your favor. Since the lender is already accepting a loss on the loan owed, it’s unlikely that they will be willing to cut prices significantly.

If you want your offer to be accepted, you should submit a reasonable offer, a sizable earnest money deposit, and a pre-approval letter. This will show the seller’s lender that you are a serious buyer. Also, include the real estate comps to show that your offer price is reasonable and data-based.

5. Negotiate the Terms

The mortgage lender has the ultimate say in who buys the property. If they reject your offer or comes back with a counteroffer, you (with the help of a real estate agent) should negotiate the sale price and contingencies. However, you should know what your limits are beforehand and be willing to walk away if the deal doesn’t make sound financial sense.

6. Seal the Deal

Once you have reached an agreement with the seller’s lender, the last step is closing. Make sure you understand all the terms of the deal and everything is in writing and duly signed.

The Bottom Line

Buying short sale real estate can be a great real estate investment strategy. However, it comes with challenges that you should be prepared for. Before you make a purchase, make sure to do your due diligence before you submit your offer. Working with an experienced real estate agent and using Mashvisor’s tools for your property search and analysis will help you find the best real estate investments.

Mashvisor provides state of the art real estate investment tools to help you make wise investment decisions and walk you through your investment journey. Please sign up here to start analysing the investment opportunities in both short trem and long term rental industry.