{kind=link}

What is a fully amortized loan? And why should you care about the answer?

If you’re looking to invest in real estate, or even if you just want to buy a house to live in, then loan amortization is something that you should definitely learn about because it will play a major role in your finances for the next number of years depending on the type and duration of the loan you want to take.

So, in this blog, I will do my best to answer the questions that you should be asking: What does fully amortized mean? what does amortization mean in real estate? And how can you calculate your amortization and factor it into your investment calculations?

Let’s find out!

What is a Fully Amortized Loan?

The short answer is: an amortized loan is a type of financing which is paid off over a set period of time in the form of monthly payments which are divided between the loan’s principal payments and the interest payments.

In other words, with an amortized loan, and unlike traditional mortgages, you don’t have to pay a big lump of money at the end of the loan’s duration. Instead, all of the loan’s amount (the principal) and the interest rate will be divided by the duration of the loan and paid on a monthly basis.

Amortization

In this sense, amortization means paying off the loan and the interest rate, but over a set period of time.

As a borrower, once you have taken an amortized loan, you will want to fully amortize the loan in order to pay off your debt. And, while you will have to pay a set amount of money to pay off your amortized loan, it doesn’t mean that you can’t do anything to hasten the process or reduce the overall money that you will have to pay.

What Does Fully Amortized Mean?

So, what is a fully amortized loan?

It’s a loan that is fully paid off – a goal that you definitely want to achieve as an investor.

And like any other type of loan, there are different variations of an amortized loan. Each variation has a different set of rules that dictate the duration and the payments that you have to make in order to fully amortize the loan.

Some loans can be fully amortized before the end of their original duration, for example. While others have interest rates that change over time, making them more volatile but have the potential of being more cost-efficient.

Related: Why Is Interest Rate on Investment Property Higher?

Options

There are a number of notable types of loans that you should be aware of:

- Interest Only Loans

- Adjustable-Rate Mortgages (ARMs)

- Fixed-Rate Loans

Interest only loans are loans that have a set period during which you only have to pay the interest rate payments. After the set period is finished, you would have to either pay the total principal amount which has accumulated during this period as a balloon or lump payment, or you would start paying higher monthly principal payments, and therefore higher monthly payments in general, for the rest of the loan’s duration.

Adjustable-Rate Mortgages are amortizing loans that have a set period (teaser period) during which the monthly payments will be fixed (meaning the interest rate and principal will not change). Once this period is over, the lender can change the interest rate (increase it or decrease it) periodically, which means your monthly payments can either increase or decrease for the remainder of the loan’s duration.

A fixed-rate loan is the most common and safest type of amortizing loan. As the name suggests, with a fixed-rate loan your monthly payments will be at a fixed amount. During the duration of a fixed amount loan, the interest rate will be a larger portion of the total payment at the beginning but will decrease gradually and the principal payment will become the larger portion of your monthly payment.

I should also note here that, in most cases, you will have the option to pay in advance a portion of the loan’s principal at any point of the loan’s duration, which will decrease your future monthly payments and the total amount of interest that you will end up paying by the time you fully amortize your loan.

Related: 10 States with the Lowest Mortgage Rates in 2021

Examples

Now that you know what is a fully amortized loan, let’s see an example of how it is calculated to further understand how it plays a major role in your finances.

Let’s suppose that you are taking a loan of $100,000 with an interest rate of 5% with an amortization duration of 5 years.

In this case, the first thing you want to do is to divide the principal amount over the duration of the loan.

So, it would be: (100,000 / 60 = 1,666.6)

This means that your monthly principal payments will be $1,666 over the duration of 60 months (5 years).

The next thing you want to do is to calculate the amount of interest rate you will be paying each month. To do so, you want to calculate the total amount of interest rate: (100,000 X 5% = $5,000)

After that, you want to divide the total amount of interest over the duration of the loan.

This would be: (5,000 / 60 = 83.3)

So, the amount of monthly payment that you need to make for the interest rate is $83.

Now, add the two amounts together and you will get the total amount of the loan’s monthly payment in order to fully amortize it.

$1,666.6 + $83.3 = $1,749.9

Of course, this calculation only works for a fixed-rate loan. In the case of adjustable-rate mortgages or interest-only loans, the calculations can be a lot different.

But it doesn’t matter. Do you know why? Because you won’t be doing the calculations manually. Like every other investor out there, you will be using a loan calculator in order to figure out your finances and whether or not you can afford the loan.

How to Calculate It as an Investor?

In addition to the hassle of the loan calculation; as an investor, you also need to factor in the property’s expenses and returns in the equation to figure out if your investment is making you money and how much money is it making.

So, what is a fully amortized loan for you as an investor?

It depends on your investment plan. If you’re planning to invest in a rental property, then you will need to factor in the rental income, property tax, maintenance costs, occupancy rates, and many other things to see the bigger picture of your finances.

A successful investment in a rental property means that the property’s rental income can cover the loan’s monthly payments. Meaning, if you factor in all the monthly expenses, including the loan’s amount, and you get a positive cash flow until you fully amortize the loan, then your investment is doing very well!

But how can you successfully calculate all of these variables and keep a sane mind at the same time?

Traditional Calculator

If you’re looking for a loan calculator that can calculate your amortizing loan and its monthly payments, there are plenty of options on the internet for you to choose from.

For example, you can use Forbes’s simple loan calculator.

However, a loan calculator is mostly used by homebuyers who want to use the property as a primary residence. This is because a homeowner doesn’t need to worry about the property’s income and how to profit from it. They just want to know the amount of monthly payments that they need to make.

You, as an investor, will need more than that.

Related: Investment Property Mortgage Rates 2021 Forecast

What Does Amortization Mean in Real Estate?

As an investor, you will need a tool that calculates the bigger picture for you.

This means that you need a calculator which can calculate your property’s finances while factoring in the amortizing loan payments.

This includes a large number of variables. You first have to calculate your property’s finances:

- Price of the property

- Its rental income (traditional and Airbnb)

- Maintenance costs

- Property management

- Property taxes

- Rental income taxes

- HOA Fees (if applicable)

- Cleaning fees

- Utilities

- Insurance

Those, in addition to other factors, all need to be calculated in order to see the total expenses vs the income that your rental property will incur.

If you want to factor in your amortizing loan amount, it needs to be part of your total expenses. Once you have all of these values, you can calculate your cash on cash return, your cap rate, and your cash flow.

If your cash flow is negative, it means that your property isn’t making enough income to cover all of the monthly expenses. However, in some cases, the cash flow might be negative for one rental strategy and positive for another.

So, where can you find a calculator which can factor in for all of the above and more, while allowing you to adjust the values on the fly and see immediate results on the short-term and long-term health of your investment?

Mashvisor’s Calculator

This is where Mashvisor’s investment property calculator and mortgage calculator come in.

Mashvisor is a real estate investment platform that is designed to help real estate investors on their investment journeys by offering them all the tools they need in order to make a successful investment in one place.

One of the tools that Mashvisor offers you is the investment property calculator – a tool that allows you to factor in all expenses affecting your property and shows you the return on investment that your property will have based on the values you enter.

The mortgage calculator is part of the property calculator. It allows you to enter the type, duration, amount, and interest rate of the loan or mortgage that you’re taking, and then calculates its monthly payments and adds them to the total expenses of your property.

You can use this tool to compare any number of properties that you find on our platform to see which one makes the most sense to you and gives you the most return on investment.

The Calculator at a Glance

To give you an idea of how the calculator works and how simple it is to use, let’s take a look at some screenshots from Mashvisor’s platform showcasing the property and mortgage calculators and how they function:

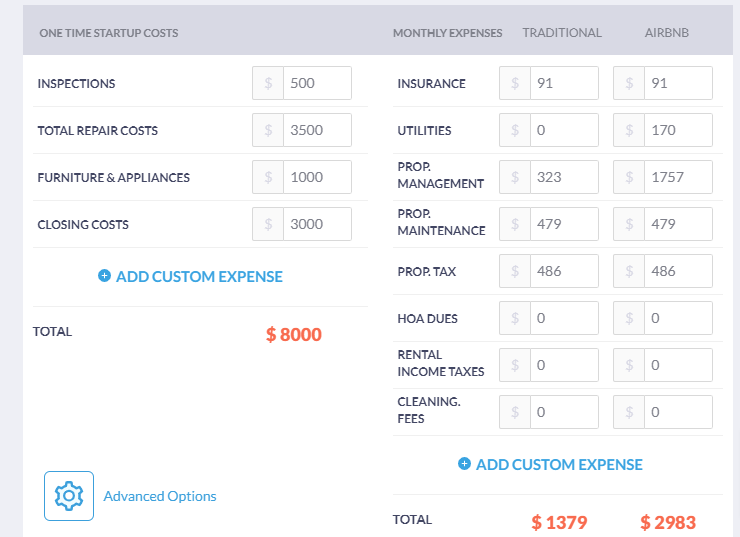

What you see here is the expenses section of the calculator. This section includes all the common recurring expenses that your property will incur.

When you open the property page for any property on Mashvisor, the values on the calculator will be pre-filled based on the property’s historical data as well as the average expenses of the area.

This means that the pre-filled values might not be 100% accurate, and it is always advised to do your research and ask an agent in the area and adjust the values on the calculator accordingly.

The calculator also gives you the option to add custom expenses if there are any.

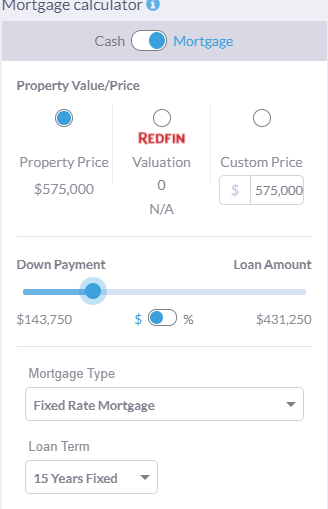

This is the mortgage calculator tool that allows you to enter the value of your loan and pick the type of loan you want to take, its duration, and its interest rate.

The mortgage calculator will calculate the loan’s monthly payments and factor them into the property’s expenses in order to give you the results.

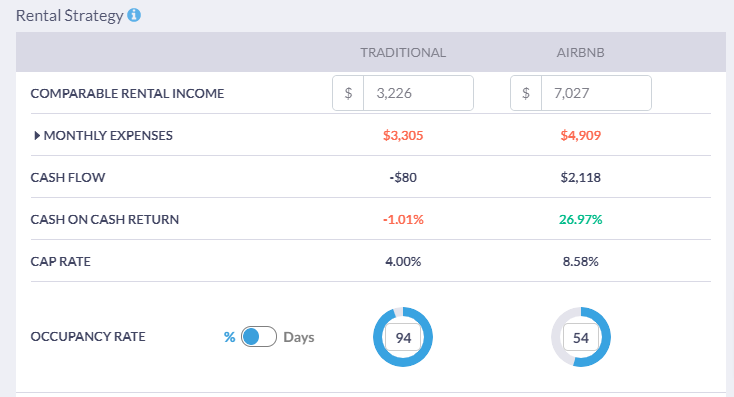

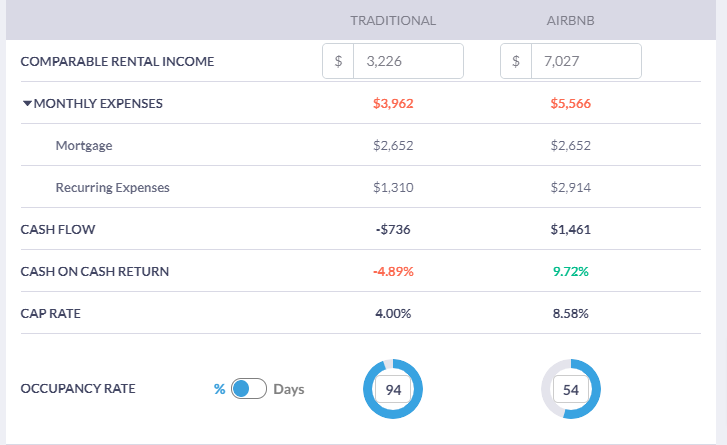

This is the results section of the calculator. It includes all the metrics that you, as an investor, need to know in order to assess the investment value of the property.

As you can see, the calculator automatically adds all of the monthly expenses, including your amortizing loan payments, and calculates them against your property’s income in order to give you the expected cash flow of the property.

Additionally, Mashvisor’s calculator will include both rental strategies, traditional long-term, and Airbnb short-term rentals, and compares them to show you the optimal rental strategy for each property based on all the values entered.

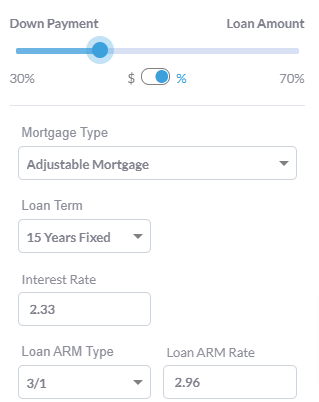

But what about Adjustable-Rate Mortgages and other types of loans with adjustable values?

As you can see, the mortgage calculator includes ARMs, and you can even choose the type of ARM and its adjustable interest rate to get an estimate of the monthly payments that you will make in the long term.

Learn more about Adjustable-Rate Mortgages (ARMs) vs Fixed-Rate Mortgages

Examples

To give you an example of how the calculator works and how the mortgage calculator will affect the results, here are two examples of a rental property’s calculator results for a 15-year and a 30-year fixed-rate amortizing loan:

Here, you can see the results for a 30-year fixed mortgage. As you can see, the property’s cash flow, in this case, is positive, which means that the rental income coming from the property is enough to cover the loan’s monthly payments as well as all other expenses that come with the property, and it even leaves you with a little amount of cash for your pocket.

Here, however, the cash flow is negative. This is because this is a 15-year fixed mortgage, so the monthly loan payments are higher, leading to a negative cash flow.

In this case, and after seeing the difference in the calculations, you can make your decision:

Do you take the 30-year mortgage and enjoy an income property that pays for itself, but end up paying a larger amount of interest rate on your loan?

Or do you take the 15-year mortgage and pay overall interest rate, but have to pay from your pocket to cover the property’s expenses and keep it running?

Most investors would choose the first option as it’s the easier and safer one. However, some investors might have other income properties with positive cash flow, which they can use to finance the expenses of this property.

Overall, and in the long term, big investors want to save as much money as they can, so they opt-in for the 15-year plan to pay less interest.

If you’re a beginner investor, however, and this is your first or second investment property, then it’s a better idea to go for the 30-year option as it will be easier for you to manage and will be a great opportunity to learn more about real estate investing without falling under the pressure of a negative cash flow property.

Conclusion

When asking “what is a fully amortized loan?”, you should be thinking about your overall finances and how an amortized loan affects the investment property you want to buy and its return on investment.

If you’re planning on taking an amortizing loan in order to purchase a rental property, then Mashvisor’s platform and property calculator are perfect for you.

Make sure to check out our website and get familiar with the tools that will help you throughout your investment journey and help you become a professional real estate investor. Start out your 7-day free trial with Mashvisor now!