{kind=link}

Real estate investors are always looking for bargains in the market. After all, the less money you pay for an investment property, the higher the ROI potential is (generally). This explains why many investors seek out foreclosed homes. Since the housing crisis of 2008, real estate investors have become familiar with foreclosures and the benefits of investing in them. However, one term that might not be as familiar is short sale. Despite being less common, real estate short sale properties offer good investment opportunities for novice investors. If you’ve never heard the term short sale, you must be wondering:

- What is a short sale property?

- What’s the difference between short sale vs foreclosure?

- What is the process of a short sale in real estate?

- What are the pros and cons of investing in a short sale property?

We’re here to answer all your questions! Keep reading to learn everything you need to know about short sales in real estate investing. Let’s start out with the short sale definition.

What Does Short Sale Mean?

Before considering buying a short sale home, it’s important for investors to know what it is and how it’s different from other types of real estate contracts. It all starts when a distressed homeowner owes more on the outstanding mortgage than the home is worth. A short sale happens when the mortgage lender (the bank), allows the property to sell for less than what the homeowner owes on the mortgage in order to facilitate a sale. In other words, the lender forgives the remaining balance of the loan in order to sell the property.

Short sales have been around for decades. However, their existence was unknown to the general public until lenders and agents began promoting the option to distressed homeowners. This made it possible for owners to market their properties as short sales before going into the foreclosure process. This is beneficial to both lenders and homeowners. Additionally, this also opened the door to new investment opportunities for real estate investors looking for a good deal on a house. So in a way, a real estate short sale can be beneficial for all parties. Here’s a typical short sale scenario:

A homeowner buys a home for $500,000 with a 10% down payment, borrowing $450,000. Five years later, the owner falls behind on the mortgage payments and decides to sell the property. However, upon conducting a comparative market analysis, he realizes that the home’s value fell to $300,000. In this example, say that the owner has taken a 30-year fixed-rate loan at 5%. So after 5 years, the loan balance would pay down the mortgage to just over $413,000. So, if the homeowner wanted to sell the property for its current value, he’d still need $113,000 more just to cover the existing mortgage. This is where a short sale comes into play if the lender agrees to the owner selling the house.

Foreclosure vs Short Sale Homes

A short sale in real estate is sometimes confused with a foreclosure. However, buying an investment property through a short sale is different from buying a foreclosed home and it’s important for real estate investors to understand how exactly. First off, the short sale occurs first when the owner attempts to sell the house and pay back the money owed on the mortgage. If he/she fails to do so, the lender takes ownership of the home and tries to sell it in order to get paid money owed.

Related: What Is a Foreclosure? How Can You Invest in One?

As a result, an owner would go through a short sale in an attempt to stop the foreclosure. This is because a short sale is viewed as a better option than going into foreclosure – for both the lender and the owner. For example, if the owner succeeded in selling the property via short sale, he/she avoids the credit hit that comes with foreclosure. In addition, banks are likely to lose less money on a real estate short sale than they would on a foreclosure. More differences between foreclosure vs short sale property include:

- Short sales are usually initiated by owners when the value of the real estate properties drops by 20% or more. On the other hand, foreclosures are initiated by the lender after the borrower fails to make the mortgage payments.

- Short sales tend to be lengthy and paperwork-intensive transactions. Foreclosures move faster and don’t take as long to complete because banks have already taken care of any outstanding liens and want to liquidate the asset ASAP.

- In some cases, a homeowner who has gone through a short sale may qualify to buy another real estate property immediately. However, because a foreclosure hits your credit score, you have to wait a minimum of 5 years to buy another property.

- While foreclosed homes close quicker than short sale homes, these properties may be in bad shape, neglected or even deliberately damaged by their previous owners.

The Short Sale Process for Sellers

Before going ahead and buying a short sale home as an investment property, a real estate investor needs to understand the short sale process first. This should help you in completing the transaction and closing the deal smoothly. As mentioned, the owner initiates the short sale – this is how the process goes:

Step 1: Identify the Current Situation

The short sale process for sellers starts once they’ve identified their current situation of lacking funds to cover their monthly mortgage payments. We should note that short sales happen as a result of increasing hardship – not due to a failure to make payments. The homeowner then requests a short sale if the burden of making their monthly mortgage payments becomes too much.

Step 2: Demonstrate Provable Financial Hardship

After identifying the current situation, homeowners have to actually prove their hardships to the bank or their lenders. So, the next step in the short sale process is to prove that payments are too hard to keep up with at their current rate. In order to be considered for a short sale, owners need to provide financial documentation that suggests they’re incapable of making future payments.

In addition, the value of the home must be less than the amount owed. A lender isn’t going to approve a short sale if there’s enough equity in the property to at least breakeven with a regular sale. So, the homeowner must be “upside-down” on the loan – meaning, they owe more on the mortgage than the home’s fair market value. So, the homeowner needs to conduct a comparative market analysis (CMA) to find the value of the property.

Related: Learn How to Do a Comparative Market Analysis Like a Pro

Step 3: Enlist the Services of a Qualified Agent

When a short sale in real estate is approved, the next step for homeowners is to contact an agent who is specialized in short sales and knows how to navigate the process efficiently. The agent will contact the lender on the seller’s behalf, have the lender send a short sale packet, and put the house for sale at the low end of fair market value.

Step 4: Gather the Appropriate Documents

Additionally, a real estate agent also helps in gathering necessary documentation that shows the owners’ current financial status and why a short sale makes sense. After all, the mortgage lender could lose money in the process. Different lenders have different document requirements for the short sale of a property, but typically, you’ll need:

- 2 months’ worth of bank statements

- Copies of your current bills and your recent income tax records

- Details about any assets you have

- Copies of your pay stubs or documentation of your unemployment

- A copy of your listing agreement

- A hardship letter detailing the circumstances surrounding your negative financial situation

Step 5: Proceed to Sell the House

After getting an offer for the short sale, send the proposal packet to your lender using certified mail. Then have your agent continually follow up with the lender. If the lender accepts the proposal, then close the deal. But if the lender rejects the deal, owners should request a reason for the rejection in writing and continually work to negotiate a transaction that is agreeable to both parties.

The Short Sale Process for Buyers

As a real estate investor, knowing how to buy a short sale house is more important to you. As mentioned, the process involves paperwork and can be lengthy. To help you get an idea of how it goes, we broke it down into the following 5 steps:

Step 1: Find and Visit the Short Sale House

The first step is obviously to start your short sale property search to find short sale listings. You can do that by checking online listings on websites like Mashvisor, searching courthouse listings, legal ads or with the help of an experienced agent.

Visit the Mashvisor Property Marketplace today to find a short sale home.

Once you find a short sale property for sale, try to determine how much is owed on the house in relation to its value. If it’s high, it could be a good deal because this indicates that the seller might have trouble selling the house for enough to satisfy the loan.

Before you make an offer on short sale real estate property, make sure to visit it in person and gauge its condition. This helps you have an estimation of how much it’s going to take to repair or renovate the investment property. If it needs a lot of work, a typical homebuyer won’t consider it. This could make it a good deal for you as a real estate investor.

Related: 14 Things to Consider Before Buying Investment Properties in 2019

Step 2: Do Your Research and Analysis

Just as with any real estate investment, you have to do your research and due diligence before buying and committing to short sale properties. First off, you should find what liens are on the property and which lender is the primary lien holder. You can ask the seller or his/her agent about this and confirm this information through a title search. This will help you ensure that there are no undisclosed liens on the property before closing the deal.

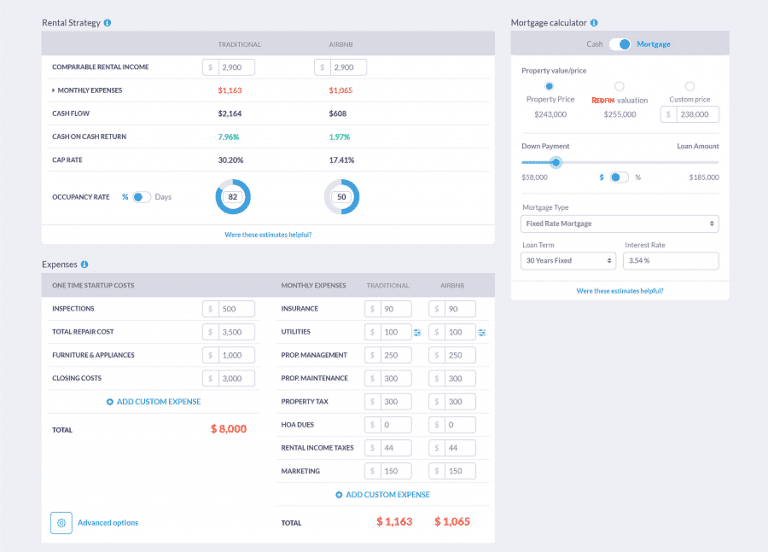

Next up, you’ll need to conduct an investment property analysis. As a real estate investor, the goal of buying short sale property is to profit from the deal. The only way to ensure that the property is actually worth it is by analyzing its potential for making money. Therefore, you should do an investment property analysis with the help of a Real Estate Investment Calculator. This tool shows you the potential return on investment in terms of rental income, cash flow, cap rate, and cash on cash return – these are numbers that every investor needs to analyze properties.

Mashvisor’s Real Estate Investment Calculator

To start looking for and analyzing the best short sale properties in your city and neighborhood of choice using Mashvisor’s investment tools, click here.

Step 3: Figure out the Financing

Once you’ve found a short sale property for sale that would be a profitable investment, start thinking of how you’ll pay for it. Unless you’re buying in cash, you need to get the lender involved. If you have a good credit score, lenders might be willing to give you a loan to speed up the short sale process. This is why it’s important to get the financing before working out an agreement with the seller. It’s common that lenders require closing in as little as 20 – 30 days once the agreement is settled. Therefore, if you wait, it’ll be too late to start shopping for a mortgage and you could lose a good deal.

Step 4: Prepare and Send Your Offer

After working out an agreement with the homeowner, have him/her sign an authorization letter which gives the lender permission to discuss the mortgage situation with you. Then, you or your agent should contact the lender and ask for a short sale package to fill in your proposal and send back to the bank which includes the authorization letter plus:

- The purchase and sale contract — signed by both the seller and buyer — to buy the property for a specified price. In most cases, you also need to post a sizable amount of money to demonstrate your ability to go through with the transaction if accepted. Without a sizable down payment, the lender would have no reason to believe you can do any better than the last owner.

- A hardship letter provided by the seller. As mentioned, lenders only accept a short sale on a house if the owner can’t make payments due to hardship and has proof that the situation is irreversible. A hardship letter that gives an overview of the seller’s desperate situation should convince the lender that taking a smaller loss now is better than a bigger loss later.

- A statement of the property’s value. This can be an appraisal or a broker’s estimated price. You want to show the lender that the seller won’t get enough for the home via a normal sale to satisfy the loan. So, the lower the estimated market value, the better it’ll be for you. Also, include a list of the problems that negatively affect the property’s value and make it undesirable to the average homebuyer.

- Detail the costs and liabilities. A real estate investor wants to show the lender that they would be much better off selling the house via short sale. So, take photos of any damages and get estimates of the repair costs. This also gives you an opportunity to take a good look at the property and decide if you’re willing and able to invest the time and money required to fix it up.

- A settlement statement. This statement can be prepared by a closing agent or real estate lawyer. It outlines the purchase price, closing costs, and any other costs or fees involved in the transfer of the short sale investment property.

Step 5: Negotiate the Terms and Seal the Deal

An investor should keep in mind that the lender may reject the offer on a short sale property or have a counteroffer. Therefore, you need to be ready to negotiate as with any real estate transaction. Figure out what your highest limit is and don’t be afraid to walk away if the lender won’t meet your figure. After everyone has reached an agreement, get everything in writing and officially recorded. Finally, the time comes for the closing and the property is yours!

The Benefits of Buying a Short Sale Home

Short sales in real estate have proven to benefit everyone involved. Homeowners no longer have to fear a foreclosure and banks are able to recoup some of the money they were promised. As for investors, here are the benefits of purchasing a short sale income property.

#1. Short Sales Have Better Prices

The primary reason for buying short sale income property is the low price. As mentioned, short sale homes are priced below market value which makes them a huge bargain and opportunity for real estate investing. In addition, banks and homeowners are motivated to find a buyer as soon as possible and will accept low offers. For them, it’s best to sell and recover some of the amount owed on the mortgage than to receive nothing and let the house sit empty.

#2. Investors Face Little Competition

Many homebuyers are not used to the short sale process and many don’t want to get involved. For a real estate investor, this is a definite plus of buying a short sale property as it means you’ll face less competition for the home. This also means you’re less likely to get caught in a bidding war that can drive up the price of the investment property, especially if you’re in a hot market.

Start looking for a short sale property right now on Mashvisor.

#3. You Can Inspect the Property

When buying a foreclosure, you may have some degree of difficulty inspecting the home and a full inspection may not even be an option. In contrast, with short sales, homeowners may allow you to bring in an inspector to inspect the property before finalizing the deal. The owner also has to provide a list of any major issues with the property that need repairs. This helps the real estate investor understand the property’s current condition before committing to the investment.

#4. Financing Is Often Available

Finally, another benefit of purchasing short sale property is that banks are more likely to finance the sale. This is because it’s in the lender’s best interest to sell quickly and avoid more debt. In addition, financing options are flexible in most cases. So, once the terms are agreed upon, the lender is likely to work with the investor buying a short sale – this is not always the case with foreclosures.

Related: How to Buy Investment Properties: Short Sale vs. Foreclosure

The Risks of Buying a Short Sale Property

While buying short sale can be a great investment opportunity, it can also have its disadvantages such as:

#1. Short Sales Can Take a Long Time

The first thing to be aware of before getting into short sale real estate is that the process is longer than a traditional home sale. How long does a short sale take to close? Some are completed in as little as a month while others could take up to a year to be finalized. Many factors influence this time table including if sellers are approved, the number of lenders involved, and the lender’s experience dealing with short sales. This can be a deal-breaker for real estate investors looking to buy investment properties quickly. Also, the lengthy short sale process could cause you to miss out on other potential properties.

#2. Short Sale Homes Are Sold “As Is”

Unlike a traditional home sale, short sale houses are sold “as is.” These properties are usually neglected and need repair. But, because lenders are already losing money on the property, buyers are unable to negotiate on price in exchange for the needed improvements, repairs, or updates. This is why it’s crucial to get a home inspection and uncover any major issues the property may have before investing your time and money.

#3. Subject to the Mortgage Lender’s Approval

Short sales can only be done if the bank agrees to take a loss on the mortgage they gave to the owner. No short sale may occur without lender approval because it is the lender (not the seller) who will be taking a loss. Therefore, negotiations are done with the lender and they’ll have the final say in whether your offer is accepted. Meaning, even if the seller accepts your offer, you can’t guarantee that the bank will. Of course, lenders are not too eager to take a loss on their loan which makes this more complicated.

Should I Buy a Short Sale Investment Property?

Now you know what a short sale is in real estate investing, how a short sale works, and how to buy a short sale property. The only question left is does buying short sale properties make for a good investment strategy? Considering the pros and cons of short sales, many believe that yes, buying a short sale investment property is a smart decision – if you know what you are getting into. Under the best circumstances, short sales can save you money and allow you to build equity fast. Just make sure to find a good investment deal first and analyze its ROI potential. This is something we can help you with!

Start out your 14-day free trial with Mashvisor now to use our tools to make smart investment decisions.